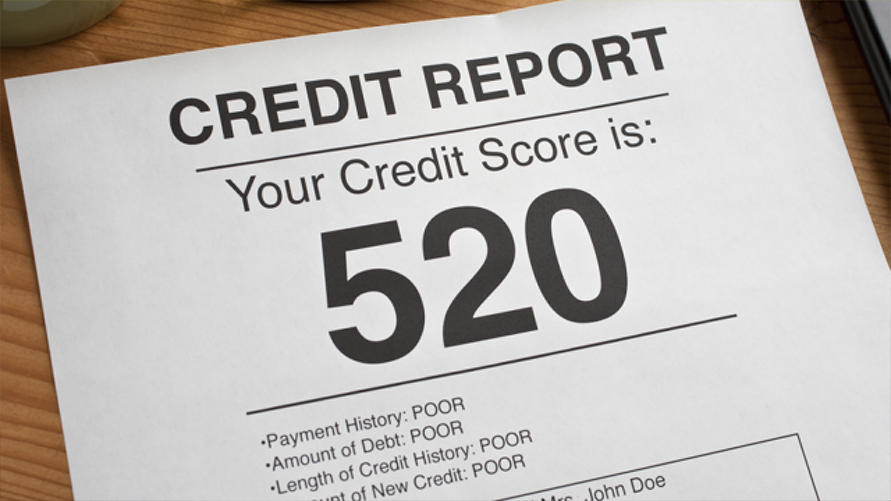

If you are looking at a credit report that a lender from a financial institution has pulled then it will also have credit scores on it, so essentially you have two different documents compiled into one report. You have the information the credit bureaus have kept on you and compiled, the credit report, then you have the credit score, which is this information taken and ran through an credit scoring model which gives you a score for the lender use in order to decide whether or not you are credit worthy to loan money to.

If you are looking at a credit report you have personally purchased then the scores you are looking at are very likely not to be FICO scores, but as we liked to say FAKO scores, the reason being they are not paying FICO to run their report through the scoring model, so they, the company you are getting your credit report from, has created an algorithm as close to what they think the FICO score is without being FICO. That is why when you look at your credit report as a consumer and you look at a credit report that is pulled by a lender your scores vary, sometimes as much as 100 points or more.